SpoorPay.

Automating cross-border payment compliance for agricultural exporters.

The problem

The agricultural sector in South Africa is one of the world's toughest. They have to deal with crumbling infrastructure, no government help and increasing regulatory burdens.

Their main source of income is international importers, but getting paid by those importers feels like a bygone era where centralised banks control everything and without a dedicated finance team smaller farming setups end up manually logging into their bank account and trying to figure out what code they need to select to declare their foreign income.

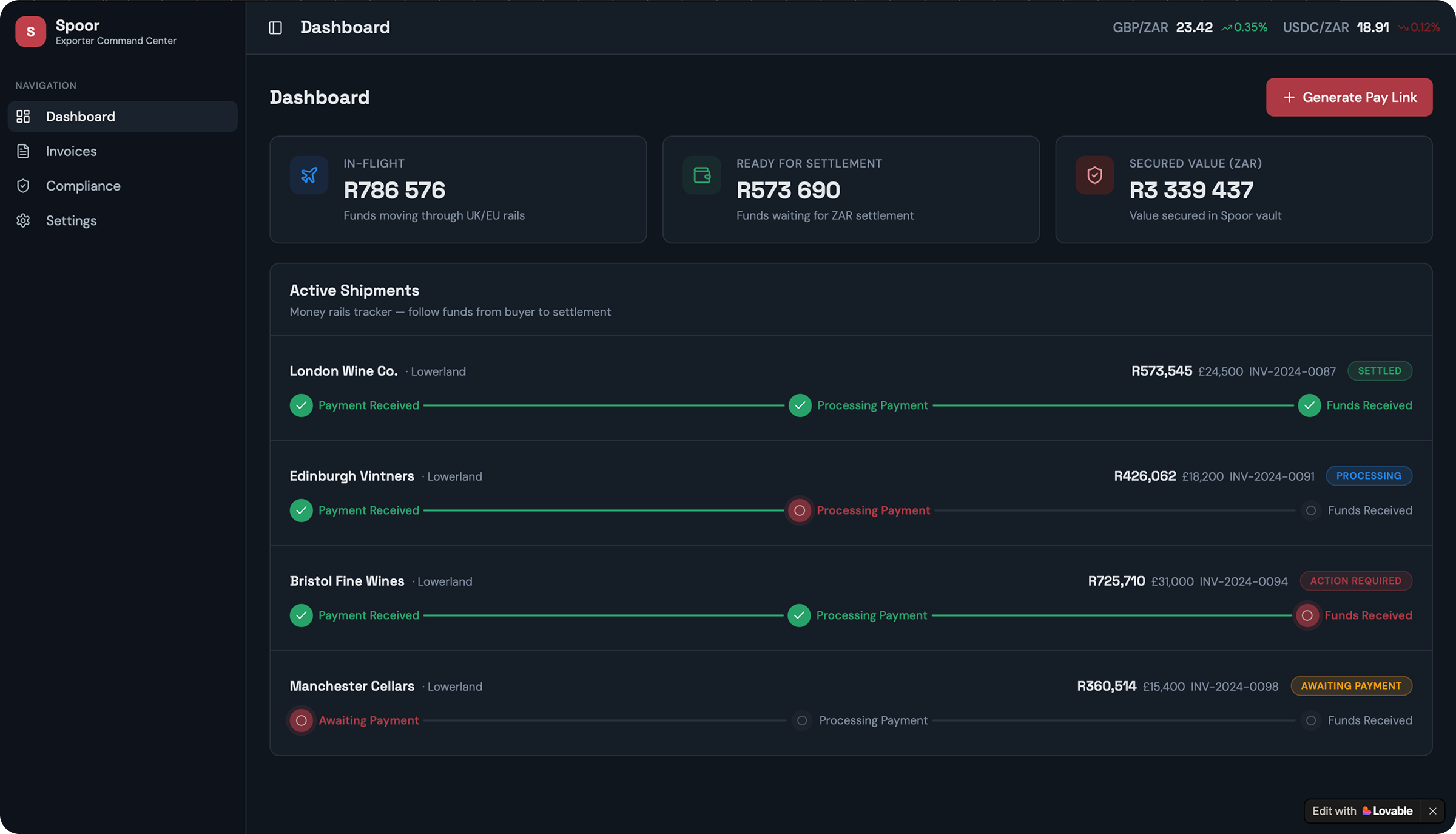

On top of that the traditional SWIFT cross-border payments rails are slow and transferring money can take days. There's no visibility on where the money is and reconciling the payment with your own books is just painful.

The opportunity

Within the world of crypto, stablecoins offer a unique opportunity in that they're pegged to the current dollar value — so no wild price fluctuations. Payments using stablecoins are also really fast, transparent and traceable from buyer to seller in real time.

However, you can't just start using stablecoins as the SA Reserve Bank has put regulations in place to make sure that it's compliant with international law.

So, are we just back to square one like SWIFT payments?

No — the opportunity lies in automating the compliance so that the farmer can focus on farming and the tech can focus on making accounting easier.

What I designed

I created SpoorPay as a design and research project exploring how crypto payments and open banking can reduce the cost and speed of receiving money for farmers, but also automating the compliance declarations for South African agri-exporters.

The visual MVP is live here: spoor-settle-hub.lovable.app

The next stage is to integrate the UI into the payment rails that I've identified that would make this not just an exploration, but a business for automating the compliance for agri-exporters in South Africa.

Why I'm building it

SpoorPay is proof that I'm not just dabbling in crypto for a job. I'm building products in the real world. I'm applying the compliance-first experience that I've used for all the fintech products that I've worked on.

I'm a believer. I know that crypto as a technology will fundamentally change the way the world moves money. And I'm excited to be a part of it.